FBR Income Tax Slabs 2025-26:

Complete Breakdown for All Categories

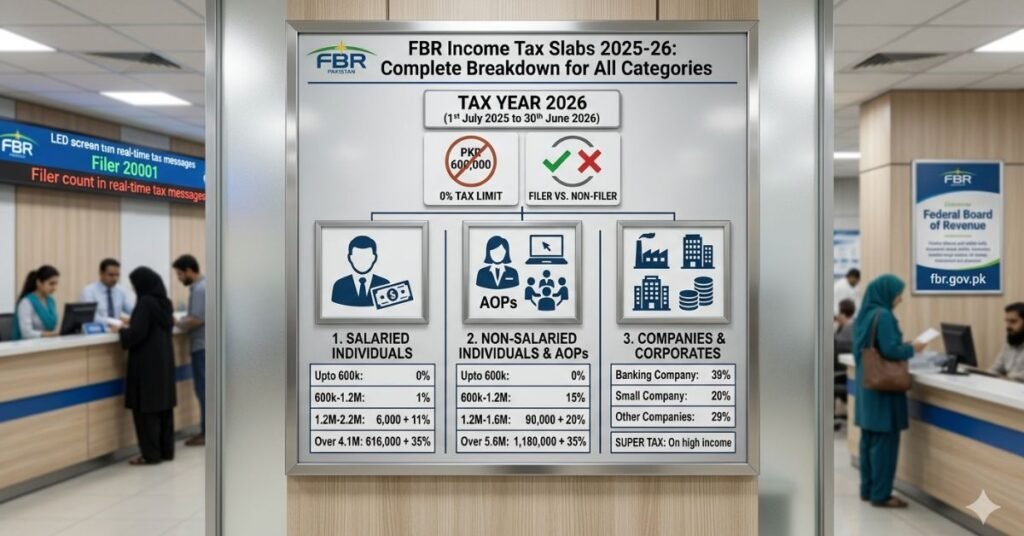

The Federal Board of Revenue (FBR) has announced revised income tax slabs for the tax year 2025-26 (assessment year 2026). Whether you are a salaried employee, business owner, freelancer, or company director — this guide breaks down every rate, threshold, and exemption in simple language so you pay exactly what you owe, and not a rupee more.

✍️ By Arshad Associates Tax Team | 📅 Tax Year 2025-26 | 🕒 ~9 min read

🏛️ Overview of FBR Income Tax 2025-26

The Finance Act 2025 brought significant restructuring to Pakistan's income tax framework administered by the Federal Board of Revenue (FBR). The new slabs are effective for the tax year running from July 1, 2025 to June 30, 2026. Key changes include revised income brackets for salaried class, enhanced surcharges on high earners, and continued incentives for IT exports and freelancers.

Understanding which slab you fall into is the first step to compliant, efficient tax filing. Pakistan follows a progressive tax system — meaning higher income is taxed at higher rates only on the portion exceeding each threshold, not on the full amount.

🧾 Not Sure Which Tax Category You Fall In?

Our certified tax consultants at Arshad Associates will assess your income sources and ensure you file accurately — maximizing refunds and minimizing liability.

👔 Salaried Individuals — Income Tax Slabs 2025-26

Salaried individuals are taxed under Section 149 of the Income Tax Ordinance 2001. The employer deducts tax at source (TDS) each month. Below are the officially notified slabs for the tax year 2025-26:

| # | Annual Taxable Income (PKR) | Tax Rate | Tax on Previous Slabs + Rate on Excess |

|---|---|---|---|

| 1 | Up to 600,000 | 0% | Nil |

| 2 | 600,001 – 1,200,000 | 5% | 0 + 5% on excess over 600,000 |

| 3 | 1,200,001 – 2,200,000 | 15% | 30,000 + 15% on excess over 1,200,000 |

| 4 | 2,200,001 – 3,200,000 | 25% | 180,000 + 25% on excess over 2,200,000 |

| 5 | 3,200,001 – 4,100,000 | 30% | 430,000 + 30% on excess over 3,200,000 |

| 6 | Above 4,100,000 | 35% | 700,000 + 35% on excess over 4,100,000 |

📊 Visual: Marginal Tax Rates — Salaried (2025-26)

Practical Example: If your annual salary is PKR 2,500,000, you pay: 0 (first 600K) + PKR 30,000 (next 600K @ 5%) + PKR 150,000 (next 1M @ 15%) + PKR 75,000 (300K @ 25%) = Total Tax: PKR 255,000 — effective rate of ~10.2%.

🏪 Non-Salaried Individuals (Business / Sole Proprietors)

Business individuals — shopkeepers, freelance professionals, consultants, landlords — are taxed under a slightly different slab structure. Note that the exemption threshold and first bracket differ from the salaried category:

| # | Annual Taxable Income (PKR) | Tax Rate | Fixed + Variable Component |

|---|---|---|---|

| 1 | Up to 600,000 | 0% | Nil |

| 2 | 600,001 – 1,200,000 | 15% | 0 + 15% on excess over 600,000 |

| 3 | 1,200,001 – 1,600,000 | 20% | 90,000 + 20% on excess over 1,200,000 |

| 4 | 1,600,001 – 3,200,000 | 30% | 170,000 + 30% on excess over 1,600,000 |

| 5 | 3,200,001 – 5,600,000 | 40% | 650,000 + 40% on excess over 3,200,000 |

| 6 | Above 5,600,000 | 45% | 1,610,000 + 45% on excess over 5,600,000 |

🤝 AOP — Association of Persons Tax Rates 2025-26

An Association of Persons (AOP) includes partnerships, joint ventures, and Hindu Undivided Families (HUFs). AOPs are taxed on total income at the following rates:

| Annual Income (PKR) | Tax Rate | Notes |

|---|---|---|

| Up to 400,000 | 0% | Exempt threshold |

| 400,001 – 1,200,000 | 10% | On excess over 400,000 |

| 1,200,001 – 2,400,000 | 15% | On excess over 1,200,000 |

| 2,400,001 – 3,600,000 | 20% | On excess over 2,400,000 |

| 3,600,001 – 6,000,000 | 25% | On excess over 3,600,000 |

| Above 6,000,000 | 35% | On excess over 6,000,000 |

Members of an AOP receive their share of profit after AOP-level tax. Individual members then include their share in personal income for rate determination purposes (but credit is given for tax already paid at the AOP level to avoid double taxation).

🏢 Corporate / Company Tax Rates 2025-26

Corporate income tax in Pakistan is governed by the Income Tax Ordinance 2001. Key rates for tax year 2025-26 are as follows:

| Entity Type | Tax Rate | Additional Notes |

|---|---|---|

| Publicly listed companies | 29% | Standard corporate rate |

| Private / unlisted companies | 29% | Same as listed |

| Small Company (turnover < PKR 250M) | 20% | Reduced rate for SMEs |

| Banking companies | 39% | Super tax applies |

| Insurance companies | 29% | Standard rate |

| IT / Software companies (export-oriented) | 0% – 1% | Final tax on export proceeds |

| Super Tax (income > PKR 300M) | +10% | Surcharge on large entities |

- Companies must file their corporate tax return within 7 months of the end of their tax year.

- Advance tax is paid in quarterly instalments based on the prior year's tax liability.

- Dividends distributed to shareholders are subject to 15% withholding tax (filers) or 30% (non-filers).

- Capital gains from listed securities are taxed separately at prescribed CGT rates.

Need help with your company's tax return? Explore our Corporate Tax Return Filing service →

💻 Freelancers & IT Exporters — Tax Rates 2025-26

Pakistan's government continues to incentivize the IT sector and freelancers through reduced tax rates to boost foreign exchange earnings. For the tax year 2025-26:

| Category | Tax Rate | Condition |

|---|---|---|

| Freelancer (remittances via banking channel) | 0.25% | Final tax on gross export proceeds |

| IT services / software exports | 1% | Final tax — registered with PSEB/SEZA |

| IT company (non-registered) | 29% | Normal corporate rate applies |

| Freelancer income from local clients | Normal Slabs | Taxed under non-salaried individual rates |

⚖️ Filer vs Non-Filer Withholding Tax Rates 2025-26

One of the strongest financial incentives to become a filer in Pakistan is the dramatic difference in withholding tax (WHT) rates across everyday transactions:

| Transaction Type | Filer Rate | Non-Filer Rate |

|---|---|---|

| Bank cash withdrawal (above PKR 50K/day) | 0.6% | 1.2% |

| Purchase of property (buyer) | 3% | 7% |

| Sale of property | 3% | 7% |

| Purchase of vehicle (above 1600cc) | 2% | 5% |

| Dividends received | 15% | 30% |

| Profit on bank deposits / savings | 15% | 30% |

| Contracts / supplies | 7% | 14% |

| Commission / brokerage | 12% | 24% |

As the table makes clear, non-filers pay 2× the withholding tax on almost every financial transaction. Becoming a filer is one of the highest-ROI financial decisions any Pakistani individual or business can make.

💼 Ready to Become a Tax Filer & Save Money?

Arshad Associates specializes in NTN registration, income tax filing, and year-round tax compliance for individuals and businesses across Pakistan.

🛡️ Key Exemptions & Allowable Deductions 2025-26

The Income Tax Ordinance 2001 provides several legitimate avenues to reduce your taxable income. Claiming these correctly can significantly lower your effective tax rate:

| Deduction / Exemption | Section | Limit / Condition |

|---|---|---|

| Zakat paid (compulsory / voluntary) | 60 | Full deduction — must be from bank |

| Workers' Welfare Fund (WWF) | – | Allowed for employers |

| Approved pension fund contributions | 63 | Up to 20% of income or PKR 1.5M |

| Life insurance premium / annuity | 62 | Proportional tax credit — 30% of premium |

| Investment in listed shares / mutual funds | 62 | Tax credit on 20% of taxable income |

| Education expenses (children) | 64B | Deduction for tuition fees paid |

| Medical allowance (salaried) | 12(2)(b) | Exempt up to 10% of basic salary |

| House rent allowance (salaried) | 12(2)(c) | Exempt up to certain thresholds |

- Keep documentary evidence of all deductions — receipts, bank statements, certificates.

- Claim Zakat deduction only if it was deducted at source (bank account) or paid voluntarily with proper documentation.

- Business owners can deduct legitimate business expenses (utilities, rent, salaries, depreciation) from gross revenue before tax.

- Losses from one head of income can be set off against profits in most cases — consult a tax professional for complex situations.

Our team can help you identify every legal deduction available to your specific situation. Learn about our Financial Planning & Analysis services →

🎯 Tax Planning Tips for 2025-26

Smart tax planning within the legal framework can make a significant difference. Here are actionable strategies for each category:

For Salaried Individuals

- Maximize pension fund contributions to reduce taxable income (up to PKR 1.5M annually).

- Invest in listed equity mutual funds to claim the Section 62 tax credit.

- Ensure your employer structures your CTC to maximize exempt allowances (medical, conveyance).

- File your return on time every year to stay on the Active Taxpayers List (ATL).

For Business Owners & Sole Proprietors

- Maintain proper books of accounts — allows you to deduct all eligible business expenses.

- Consider structuring as a Small Company (Pvt. Ltd.) if turnover < PKR 250M — pays only 20% vs 45% max individual rate.

- Claim depreciation on business assets to reduce taxable profit each year.

- Register for Sales Tax if applicable — keep input/output tax records clean.

For Companies & AOPs

- Pay advance tax on time to avoid default surcharge of 16% per annum.

- Leverage R&D tax credits and industrial undertaking exemptions where applicable.

- Conduct annual financial modeling to forecast tax liability and optimize cash flow.

- Ensure all WHT (withholding taxes) are deducted and deposited on time to avoid penalties.

❓ Frequently Asked Questions (FAQs)

🔗 Related Articles You Should Read

Deepen your understanding of Pakistan's tax system with these guides from Arshad Associates:

🚀 File Your Taxes Correctly This Year — Let the Experts Handle It

From individual tax filing and NTN registration to corporate returns and payroll — Arshad Associates provides end-to-end tax compliance solutions across Pakistan. Get in touch today for a free consultation.